On the morning of 28 February 2026, after lengthy preparations, Israel and the US launched missile strikes against Iran. The focus was on government buildings in Tehran. As things stand, these are not just pinpricks, but the beginning of a prolonged military operation against the Iranian mullah regime and its nuclear program. Iran has launched counterattacks, firing missiles toward Israel and, it appears, American military bases.

What can be said with caution at this point is that Iran’s economic weight is small. Its share of global economic output has fallen to around 0.4%. In the mid-1980s, it was still just under 1.5%. This means that Iran has slipped from 17th to 44th place among the world’s largest economies. Its share of global imports and exports is less than 0.4% in each case. Based on these figures, Iran is largely insignificant for the global economy. The focus is on Iran’s vast oil wealth. With a share of around 12% of global oil reserves, Iran ranks third behind Venezuela and Saudi Arabia. In terms of production, however, the country ranks only ninth, with a global share of 3-4%. The main buyers of Iranian oil are countries in Asia, especially China.

In addition, Iran is located on the Strait of Hormuz, which is important for shipping. Around a quarter of global oil trade passes through the Strait of Hormuz. However, a blockade by Iran would also be politically and economically dangerous for the country itself.

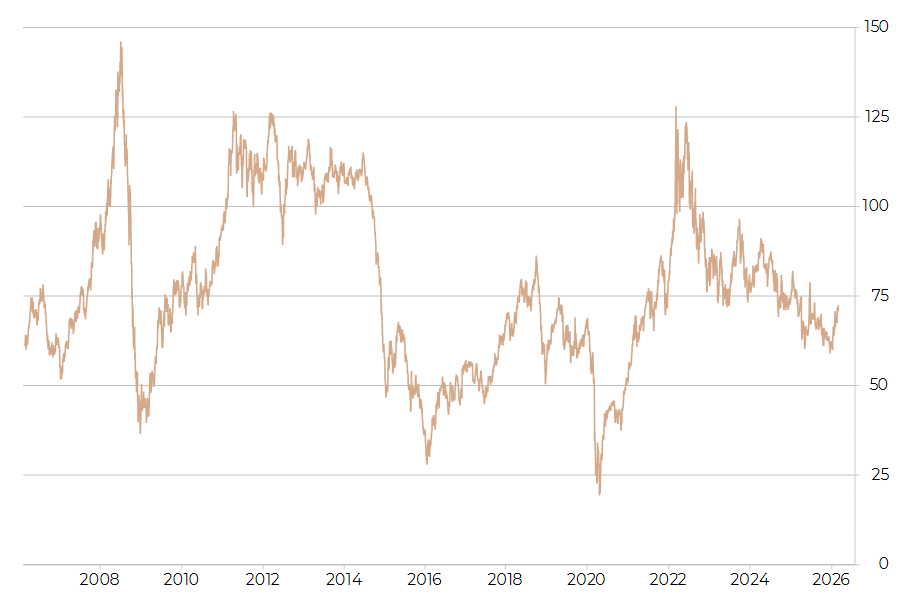

The global economy is generally most vulnerable to oil price changes triggered by the war. Off-exchange indications show an increase from around USD 73 to just under USD 80 per barrel. This is considerable, but even after such an increase, the oil price would still be at a moderate level (Fig. p. 2). If the price continues to rise, this could cause the inflation rate to increase in the short term. In the eurozone and Switzerland, however, the inflationary environment is currently relaxed, meaning that the ECB and the SNB would not need to change their monetary policy course for the time being. In the United Kingdom and the US, the disinflation process could slow down and inflation rates, which are still too high, could persist for longer. This could delay the next interest rate cuts by the two central banks.

Overall, the purely global economic consequences of the war are likely to remain manageable for the time being. However, the war is taking place at a time when the world is already facing a number of risk factors.

Within the bank’s investment committees, the geopolitically changed situation due to the current developments is already being analyzed since this morning. The bank’s house view (currently: neutral equity and bond positioning, overweight in gold) will be adjusted or confirmed by the start of trading on Monday.

Brent oil price in USD

Source: Macrobond