- As expected, the US Federal Reserve has lowered its federal funds rate by 0.25 percentage points despite persistently high inflation rates.

- With a new chair taking office in May 2026, the Fed is likely to continue its easing policy.

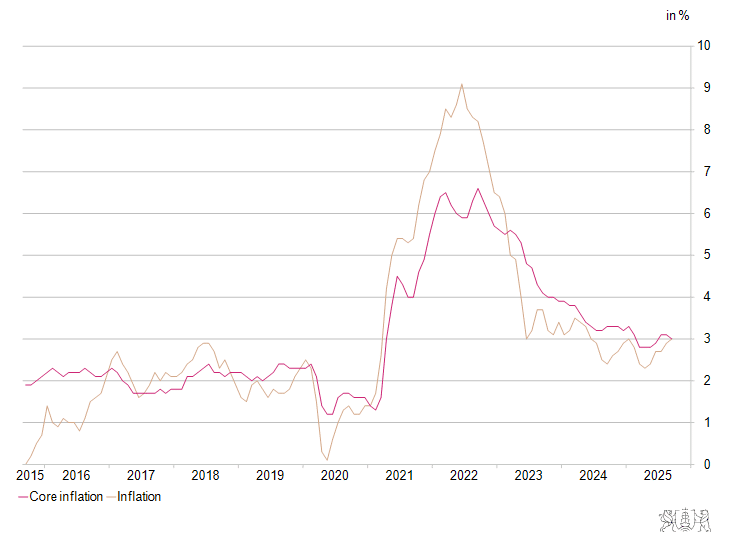

For the US Federal Reserve, the December monetary policy meeting took place in an unusual environment. At around 3%, the inflation rate is still significantly too high. Due to the government shutdown, which has now ended, the availability of economic data necessary for assessing the monetary policy situation was still limited. For example, the labor market data for October is still missing. Overall, however, the available news from the labor market paints a mixed picture. At the last Fed meeting at the end of October, the members of the Federal Open Market Committee (FOMC) were already divided on the appropriate monetary policy course. In addition, the US Federal Reserve is undergoing a personnel shake-up. Fed Chairman Jerome Powell’s term ends in May 2026. US President Donald Trump has already decided on a successor, according to his own statement – it will most likely be Trump loyalist Kevin Hassett. Regardless of this personnel change, political pressure on the Fed remains high.

In this complicated environment, market expectations for a rate cut of 25 basis points were just under 90% – and the Fed acted accordingly. The fed funds rate is falling from 3.75-4.00% to 3.50-3.75%. In addition, the Fed will initiate purchases of shorter-term Treasury securities to keep money market rates within the target range.

The Fed justifies the rate cut with the increased risks for the labor market. Inflation has risen significantly, mainly due to tariff policy. Without the tariffs, the inflation rate would be only slightly above 2%, according to Jerome Powell. Since, according to the Fed, the tariffs are causing only an one-off upward shift in price levels, the inflation rate will weaken again over time. Therefore, the downside risk to the labor market is currently greater than the upward risk to the inflation rate. The new macroeconomic projections indeed show that the Fed expects a significant decline in inflation for the coming year, with PCE inflation falling from 2.9% to 2.4% at the end of next year. The Fed has raised its GDP projection for 2026 by a surprisingly large margin to 2.3% (previously 1.8%). When asked, Jerome Powell justified this growth optimism with robust consumer spending, high investment in the AI sector, and higher productivity. The growth optimism is somewhat at odds with concerns about the labor market.

The decision on the interest rate move was not unanimous: two members voted to maintain the previous rate, while one member voted for a larger rate cut of 50 basis points.

Outlook for 2026

The US Federal Reserve is likely to continue its cutting cycle in the coming year. If Kevin Hassett becomes the new Fed chairman, which is almost certain, further monetary easing is likely. Hassett is not only considered a Trump loyalist, he also wants high stock valuations and robust capital markets. He sees high productivity gains from the AI revolution, which would dampen inflationary pressures. Following today’s rate cut, two to three further cuts of 25 basis points each could follow in 2026. As things stand at present, however, the Fed is likely to pause in the first quarter.

The Fed’s next interest rate decision is scheduled for 28 January 2026.

US inflation

Source: Macrobond.